Headquartered in Fort Myers, Florida, Conor Acquisitions is a real estate investment company primarily focused on income producing real estate within the hospitality industry. Conor concentrates on all facets of the hotel industry, including acquisition, development, construction, renovation, asset management and property analysis. Its experience ranges from urban high-rise branded hotels to boutique properties. It has worked with many hotel brands within the industry, including Hilton, Marriott, IHG, Starwood, Hyatt, Choice, Wyndham, and Best Western. Since inception, it has completed $59 million in hospitality-related acquisitions.

Conor Acquisitions aims for growth through vision, integrity, and values. It is dedicated to ensuring that its hotels exceed the expectations of their guests, employees, investors, and their partners within the community. It persistently strives to achieve superior value, provide exceptional guest service, maintain an environmentally-conscious operation and utilize advanced technologies. It is Conor's objective to increase operating efficiencies and create value-added improvements that translate to its guests.

Conor has a conservative approach to maximize ROI using its seasoned knowledge from the hospitality industry. It is well versed in legal strategies and creative solutions allowing them the capabilities to provide high profit margins for their investors. Through its efforts, Conor’s investors have often received favorable returns on invested capital .

Investment Approach

Conor Acquisitions is a motivated, growth-oriented company. The following represent target investments for Conor:

- Franchised Hotels: Marriott, Hilton, Hyatt, Starwood, IHG, Choice, Best Western, Wyndham

- Full, Select, Limited Service and Extended Stay Hotels

- Purchase price points targeted at discounts to replacement costs

- Value creation opportunities: Legal strategies and repositioning

The strategy employed on these target investments varies by which of the three categories below best applies:

Core Investments: Conor targets properties across a plethora of markets with attractive valuations, providing above average, sustainable yields and favorable long-term prospects, based on a variety of demand generators.

Value-Added Investments: Conor pursues opportunities where it can leverage their industry knowledge, relationships, and reputation to create and add value. It aims to acquire properties with upside potential, and utilize strategies such as repositioning, conversion, or redevelopment.

Opportunistic Investments: Conor welcomes opportunities where capital constraints, or the markets at large prevent an operating partner from leveraging the full potential of an asset. It explores opportunities including diversification by investing in different areas of the capital stack.

Track Record

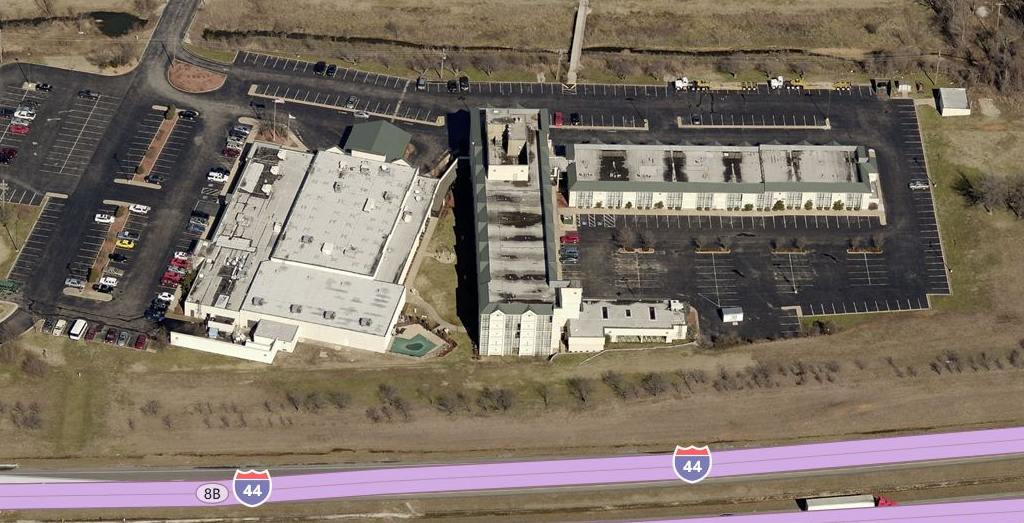

| Address: | 3615 Range Line Rd., Joplin, MO 64804 |

| Year Built: | 1979 |

| Property Type: | Hospitality |

| Number of Rooms: | 262 rooms (185 rooms Post Renovation) |

| Number of Stories: | Five |

| Parking: | 369 surface spaces |

| Major Amenities: | Day Spa Two Restaurants Fitness center Business center Indoor & Outdoor Pools Laundry facilities |

Property Highlights

- Built in 1979, the Property is a full-service, interior corridor, atrium design hotel with 262 rooms for rent contained in both a two- and five-story building. As part of HWI's requirements to obtain the DoubleTree by Hilton flag, the Sponsor plans to demolish the two-story building upon completion of renovations to the five-story tower, which will reduce the number of rooms for rent at the Property to 185.

- Adjacent and attached to the five-story tower is the commercial building which contains two restaurants, the registration lobby, atrium, business center, a leased day spa, an outdoor pool and 17,500 SF of flexible meeting and banquet space.

- The indoor pool and exercise room are self-contained in a separate building attached to the back of the five-story tower.

- The Property sits on a 9.37 acre parcel with Interstate 44 frontage.

The information on this Page is qualified in its entirety by reference to the more complete information about the offering contained in the Sponsor’s Investment Documents. The information on this Page is not complete and subject to change at the Sponsor’s discretion at any time up to the closing date. The Sponsor’s Investment Documents and supplements thereto contain important information about the Sponsor’s offering including relevant investment objectives, the business plan, risks, charges, expenses, and other information, which you should consider carefully before investing. The information on this Page should not be used as a basis for an investor’s decision to invest.

Risk of InvestmentThis investment is speculative, highly illiquid, and involves substantial risk. There can be no assurances that all or any of Sponsor’s assumptions, expectations, estimates, goals, hypothetical illustrations, or other aspects of Sponsor’s business plans (“Assumptions”) will be true or that actual performance will bear any relation to Sponsor’s Assumptions, and no guarantee or representation is made that Sponsor’s Assumptions will be achieved. If Sponsor does not achieve its Assumptions, your investment could be materially and adversely affected. A loss of part or all of the principal value of your investment may occur. You should not invest unless you can readily bear the consequences of such loss. Sponsor’s Assumptions should not be relied upon as the primary basis for your decision to invest.

No Reliance on Forward-Looking Statements; Sponsor AssumptionsSponsor is solely responsible for statements made concerning forward-looking statements and Assumptions, which apply only as of the date made, are preliminary and subject to change, and are expressly qualified in their entirety by the disclosures and cautionary statements included in Sponsor’s Investment Documents, which you should carefully review. Sponsor is obligated to update or revise such forward-looking statements or Assumptions to reflect events or circumstances that arise after the date made or to reflect the occurrence of unanticipated events. Sponsor’s forward-looking statements and Assumptions are hypothetical, not based on actual investment achievements or events, and are presented solely for purposes of providing insight into the Sponsor’s investment objectives, detailing Sponsor’s anticipated risk and reward characteristics, and establishing a benchmark for future evaluation of actual results; therefore, they are not a predictor, projection, or guarantee of future results. You should not rely on Sponsor’s forward-looking statements as a basis to invest.

Importantly, we do not adopt, endorse, or provide any assurance of returns or as to the accuracy or reasonableness of Sponsor’s Assumptions or forward-looking statements.

No Reliance on Past PerformanceAny description of past performance is not a reliable indicator of future performance and should not be relied upon as the primary basis to invest.

Sponsor’s Use of DebtA substantial portion of the total cost of the real estate asset acquired by the Sponsor with investor funds (“Property”) will be paid with borrowed funds, i.e., debt. Sponsor’s estimated rates and terms of the debt financing are subject to lender approval, and there is no assurance that the Sponsor will secure debt at the rates and terms presented on this Page or in the Sponsor’s Investment Documents, or at all. The use of borrowed money to acquire real estate is referred to as leveraging, which can amplify losses and could result in lender foreclosure. In addition, if the debt includes a variable (or “floating”) interest rate, the total amount of interest paid over the term of the debt will fluctuate and can increase. As a result, Sponsor’s use of debt can result in a loss of some or all of your investment.

Sponsor’s Offering is Not RegisteredSponsor’s securities offering will not be registered under the Securities Act of 1933, as amended (the “Securities Act”), in reliance upon the exemptions from registration pursuant to Rule 506(c) of Regulation D as promulgated under the Securities Act (“Private Placement”). In addition, the offering will not be registered under any state securities laws in reliance on exemptions from state registration. Such securities (your ownership interests) are subject to restrictions on transferability and resale and may not be transferred or resold except as permitted under applicable state and federal securities laws pursuant to registration or an available exemption. All Private Placements on the Platform are intended solely for “Accredited Investors,” as that term is defined in Rule 501(a) under the Securities Act.

No Investment AdviceNothing on this Page should be regarded as investment advice (either with respect to a particular security or regarding an overall investment strategy), a recommendation, an offer to sell, or a solicitation of or an offer to buy any security. Advice from a securities professional is strongly advised to understand and assess the risks associated with real estate or private placement investments.

1031 Exchange RiskInternal Revenue Code Section 1031 (“Section 1031”) contains complex tax concepts and certain tax consequences may vary depending on the individual circumstances of each investor. You should consult with and rely on your own tax advisor about the tax aspects with respect to your particular circumstances.