Brennan Investment Group, LLC (“Brennan Investment Group” or the “Company”) is a private real estate investment company headquartered in Chicago, Illinois. Brennan Investment Group was formed in 2010. Its Managing Principals are comprised primarily of former First Industrial Realty Trust (NYSE: FR) founders and executives. Since 2010, the Company has purchased more than $800 million in industrial real estate, partnering with institutional capital providers such as California State Teachers Retirement System (CalSTRS), Gatehouse Bank and DLJ Real Estate Capital Partners.

The Company’s current portfolio spans 21 states, encompasses over 12.8 million square feet (with an additional 3 million under management), and currently has an occupancy rate of 98.7%. Brennan Investment Group acquires, develops and operates industrial real estate in select major metropolitan markets throughout the United States, including Central Florida, Chicago, Northern New Jersey, Southern California, Texas and Washington, D.C. The Company’s experienced principals utilize a disciplined investment approach in selectively identifying opportunities that look to achieve risk-adjusted returns for investors. Brennan Investment Group believes that industrial real estate is a large, stable and diversified investment class that offers a compelling opportunity for both current income and appreciation across a variety of industrial property types.

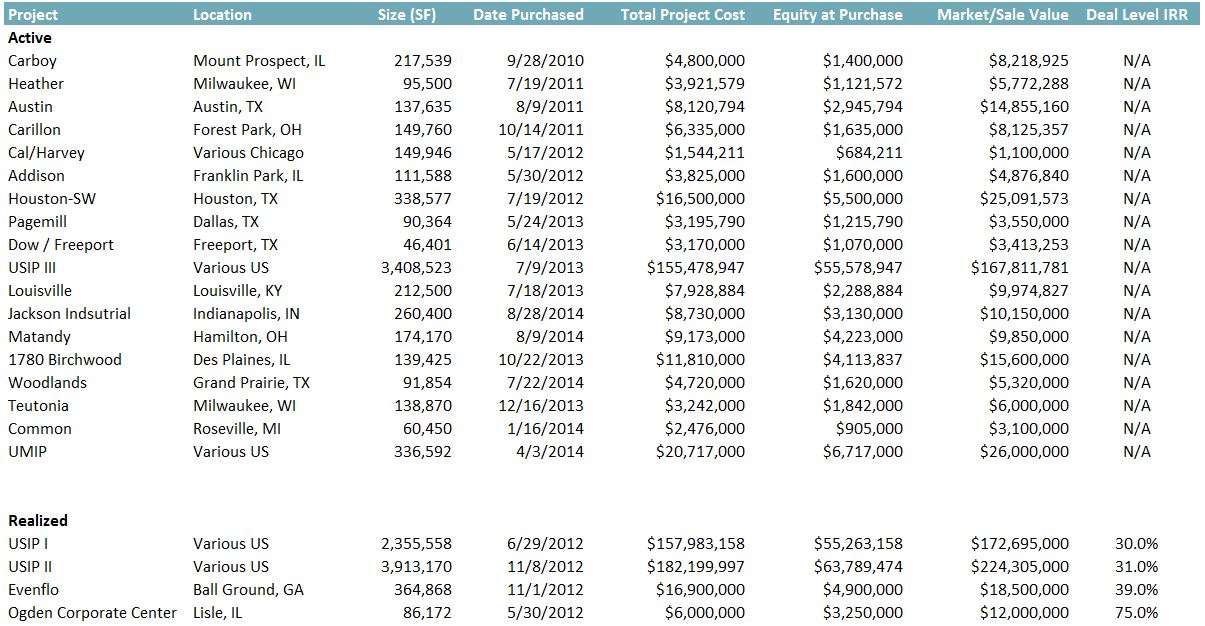

Track Record

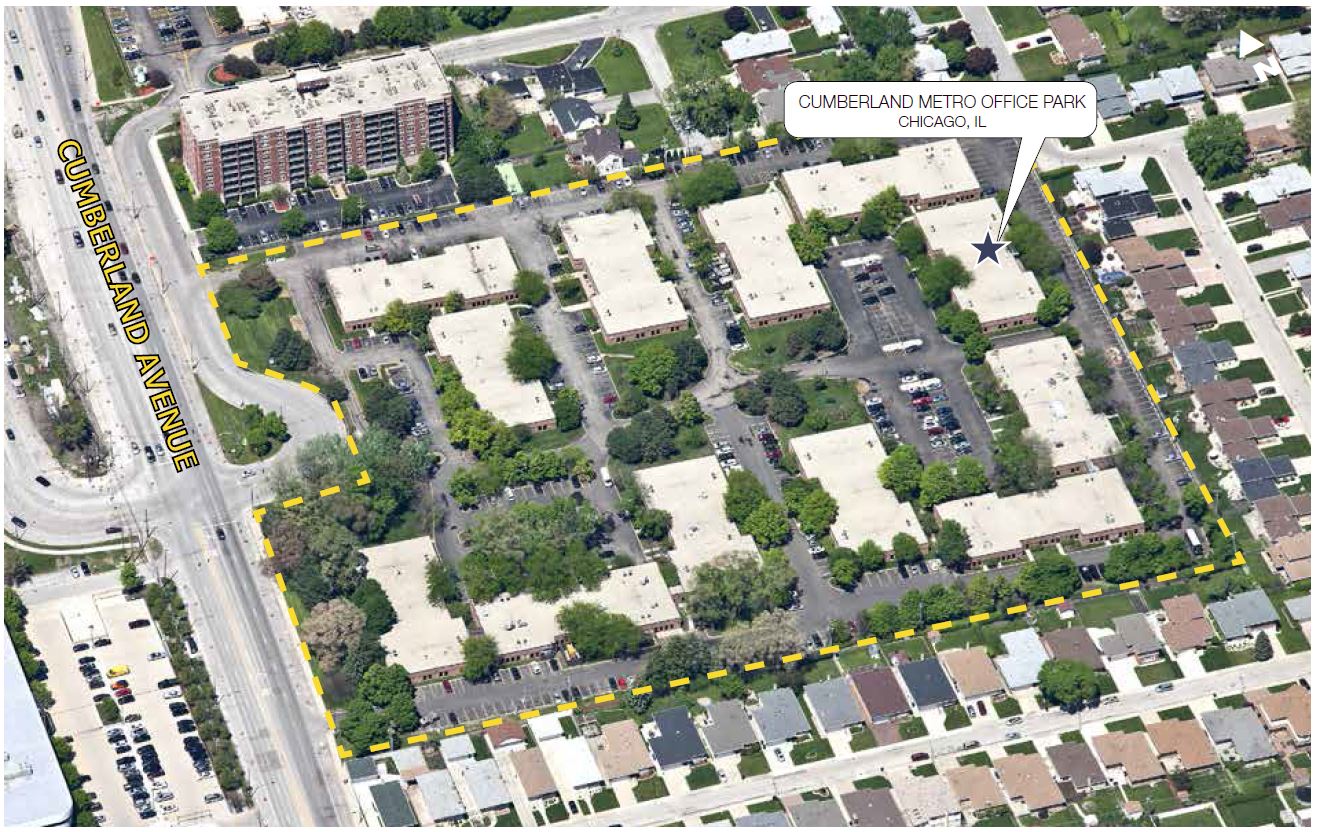

| Address: | 5501-5523 Cumberland Avenue Chicago, IL 60656 |

| Submarket: | O'Hare |

| Year Built: | 1984 |

| Current Occupancy: | 90% |

| Net Rentable Area: | 164,448 square feet |

| Total Units: | 40 |

| Parking: | 538 spaces, 3.3 per 1,000 square feet of rentable area |

Property Highlights

- Single Story Office Product: Per conversations with market professionals, tenants in the market have embraced the single story office product as opposed to traditional mid/high rise office space for a variety of reasons. Single story office offers tenants the ability to create more of a brand/tenant identity than would be possible in a mid/high rise building. Tenants enjoy the ease of access provided, including the ability for tenants/customers of the tenants to park in front of their building and walk inside, especially due to the limited parking options in the area, and particularly for the tenants involved in the medical services industry. Lastly, the rents are lower at a single story office building as there is less expense leakage, and the NNN’s (expenses billed back to the tenants) are lower, providing cost-conscious tenants an alternative to traditional office product.

- Institutional Ownership: The Property is in good condition and has benefited from institutional ownership and management, as Invesco has owned the Property for the past 15 years.

The information on this Page is qualified in its entirety by reference to the more complete information about the offering contained in the Sponsor’s Investment Documents. The information on this Page is not complete and subject to change at the Sponsor’s discretion at any time up to the closing date. The Sponsor’s Investment Documents and supplements thereto contain important information about the Sponsor’s offering including relevant investment objectives, the business plan, risks, charges, expenses, and other information, which you should consider carefully before investing. The information on this Page should not be used as a basis for an investor’s decision to invest.

Risk of InvestmentThis investment is speculative, highly illiquid, and involves substantial risk. There can be no assurances that all or any of Sponsor’s assumptions, expectations, estimates, goals, hypothetical illustrations, or other aspects of Sponsor’s business plans (“Assumptions”) will be true or that actual performance will bear any relation to Sponsor’s Assumptions, and no guarantee or representation is made that Sponsor’s Assumptions will be achieved. If Sponsor does not achieve its Assumptions, your investment could be materially and adversely affected. A loss of part or all of the principal value of your investment may occur. You should not invest unless you can readily bear the consequences of such loss. Sponsor’s Assumptions should not be relied upon as the primary basis for your decision to invest.

No Reliance on Forward-Looking Statements; Sponsor AssumptionsSponsor is solely responsible for statements made concerning forward-looking statements and Assumptions, which apply only as of the date made, are preliminary and subject to change, and are expressly qualified in their entirety by the disclosures and cautionary statements included in Sponsor’s Investment Documents, which you should carefully review. Sponsor is obligated to update or revise such forward-looking statements or Assumptions to reflect events or circumstances that arise after the date made or to reflect the occurrence of unanticipated events. Sponsor’s forward-looking statements and Assumptions are hypothetical, not based on actual investment achievements or events, and are presented solely for purposes of providing insight into the Sponsor’s investment objectives, detailing Sponsor’s anticipated risk and reward characteristics, and establishing a benchmark for future evaluation of actual results; therefore, they are not a predictor, projection, or guarantee of future results. You should not rely on Sponsor’s forward-looking statements as a basis to invest.

Importantly, we do not adopt, endorse, or provide any assurance of returns or as to the accuracy or reasonableness of Sponsor’s Assumptions or forward-looking statements.

No Reliance on Past PerformanceAny description of past performance is not a reliable indicator of future performance and should not be relied upon as the primary basis to invest.

Sponsor’s Use of DebtA substantial portion of the total cost of the real estate asset acquired by the Sponsor with investor funds (“Property”) will be paid with borrowed funds, i.e., debt. Sponsor’s estimated rates and terms of the debt financing are subject to lender approval, and there is no assurance that the Sponsor will secure debt at the rates and terms presented on this Page or in the Sponsor’s Investment Documents, or at all. The use of borrowed money to acquire real estate is referred to as leveraging, which can amplify losses and could result in lender foreclosure. In addition, if the debt includes a variable (or “floating”) interest rate, the total amount of interest paid over the term of the debt will fluctuate and can increase. As a result, Sponsor’s use of debt can result in a loss of some or all of your investment.

Sponsor’s Offering is Not RegisteredSponsor’s securities offering will not be registered under the Securities Act of 1933, as amended (the “Securities Act”), in reliance upon the exemptions from registration pursuant to Rule 506(c) of Regulation D as promulgated under the Securities Act (“Private Placement”). In addition, the offering will not be registered under any state securities laws in reliance on exemptions from state registration. Such securities (your ownership interests) are subject to restrictions on transferability and resale and may not be transferred or resold except as permitted under applicable state and federal securities laws pursuant to registration or an available exemption. All Private Placements on the Platform are intended solely for “Accredited Investors,” as that term is defined in Rule 501(a) under the Securities Act.

No Investment AdviceNothing on this Page should be regarded as investment advice (either with respect to a particular security or regarding an overall investment strategy), a recommendation, an offer to sell, or a solicitation of or an offer to buy any security. Advice from a securities professional is strongly advised to understand and assess the risks associated with real estate or private placement investments.

1031 Exchange RiskInternal Revenue Code Section 1031 (“Section 1031”) contains complex tax concepts and certain tax consequences may vary depending on the individual circumstances of each investor. You should consult with and rely on your own tax advisor about the tax aspects with respect to your particular circumstances.