Weaver Capital Partners is a private investment firm that is active in acquiring commercial real estate across the Southeast. The firm seeks opportunistic and value‐add transactions across most major property types including office, industrial, retail and mixed‐use projects. The company has been involved in six investments representing more than $185 million of total capitalization.

The Property is a two-building portfolio of adjacent buildings located in downtown Durham, less than two miles from Duke University. The buildings were originally built in 1930 and 1932, then renovated in 2001 and 2005.

Triangle Biotechnology Center, or 323 Foster Street, was originally built in 1932 as Clark & Sorrell Garage, and was the oldest repair garage still in operation in the city when it was closed in 2000. The functional brick and concrete building is listed on the National Register of Historic Places and benefits from a 50% abatement on property taxes. In 2001, after extensive renovations, Triangle Biotechnology Center was opened to address a need for R&D facilities in downtown Durham with lab space. The historic building with modern lab and office space are designed to meet the functional requirements of a broad range of different types of research. The laboratories are designed around a central utility spine that provides easy access to all major building services.

401 Foster Street was originally constructed as a warehouse likely used by Liggett and Myers Tobacco Company. In the 1940s, the building was converted to auto service and sales at which time the interior posts were removed, the roof re‐supported by steel trusses and the front façade was converted to stucco. Later, the building became home to Southeastern Radio Supply and the land continues to be owned by a trust that evolved from Southeastern Radio. The redevelopment of 401 Foster Street into the destination spot it is today commenced in 2005 with new plumbing, electrical, HVAC, storefronts, exterior stucco and signage transforming the building while striving to maintain historical integrity.

Major Tenants

[[{"fid":"33863","view_mode":"default","type":"media","field_deltas":{},"attributes":{"height":"400","width":"400","style":"width: 125px; height: 125px;","class":"media-element file-default","data-delta":"1"},"fields":{}}]]

Duke University (S&P AA+) has been a tenant at 323 Foster Street ("Triangle Biotechnology Center") since 2009. They recently exercised their first renewal option to extend the lease through 2020 and still have a second, five‐year renewal option remaining.

Duke University is a private research university with over 14,850 students as of Fall 2014. Duke consistently ranks as one of the top universities in the United States. In September 2015, CollegeFactual.com named Duke the 3rd best college for four‐year undergraduate programs ‐ beating out Stanford, Harvard and Princeton. Duke ranked eighth for best graduate school and medical programs by US News & World Report.

Duke’s research expenditures in the 2013 fiscal year were approximately $993 million, the eighth largest in the nation. In addition to its campuses spanning over 8,600 acres, Duke University occupies an estimated 1 million SF of space in downtown Durham according to Duke's head of real estate, including space at American Tobacco, Carmichael building (within Durham ID) and Triangle Biotechnology Center.

The Duke space within Triangle Biotechnology Center was designed to accommodate research which is currently led by Dr. Levin, as the Chief of the Neurobehavioral Research Lab in the Psychiatry Department, who rides his bike to work. The three main research components of his laboratory are focused on the themes of the basic neurobiology of cognition and addiction, neurobehavioral toxicology and the development of novel therapeutic treatments for cognitive dysfunction and substance abuse. Funding for Dr. Levin’s research comes from multiple sources including the EPA and NIEHS. The lab is used by both undergraduate and graduate students.

Site Plan

[[{"fid":"33852","view_mode":"default","type":"media","field_deltas":{},"attributes":{"height":"666","width":"1046","style":"width: 600px; height: 450px;","class":"media-element file-default","data-delta":"2"},"fields":{}}]]

Surrounding Developments

[[{"fid":"34127","view_mode":"default","type":"media","field_deltas":{},"attributes":{"height":"866","width":"938","style":"width: 600px; height: 450px;","class":"media-element file-default","data-delta":"3"},"fields":{}}]]

[[{"fid":"34121","view_mode":"default","type":"media","field_deltas":{},"attributes":{"height":"178","width":"229","style":"width: 225px; height: 175px;","class":"media-element file-default","data-delta":"4"},"fields":{}}]]

1. Liberty Warehouse

Previously the location of a historic tobacco warehouse, Liberty Warehouse contains 246 luxury apartments including a pool and fitness center, over 24,000 SF of retail/commercial space and a bowling alley/entertainment complex.

[[{"fid":"34123","view_mode":"default","type":"media","field_deltas":{},"attributes":{"height":"178","width":"229","style":"text-align: justify; width: 225px; height: 175px;","class":"media-element file-default","data-delta":"5"},"fields":{}}]]

2. The Chesterfield

Located by West Village on W. Main Street, The Chesterfield is a 7-story, 284,000 SF adaptively reused historic building, which will focus on life science and technology and include office, lab and retail space with a large atrium to encourage collaboration and networking. The project is expected to be completed in first quarter 2017.

[[{"fid":"34124","view_mode":"default","type":"media","field_deltas":{},"attributes":{"height":"258","width":"334","style":"width: 225px; height: 174px;","class":"media-element file-default","data-delta":"6"},"fields":{}}]]

3. City Center

City Center will be located in the heart of the City Center District of downtown Durham. It is a planned 28-story mixed use tower anticipated to include residential condos, luxury apartments, Class A office space and street level retail. The proposed building would be the tallest building in Durham, and is expected to be completed in second quarter 2017.

[[{"fid":"34125","view_mode":"default","type":"media","field_deltas":{},"attributes":{"height":"178","width":"229","style":"width: 225px; height: 175px;","class":"media-element file-default","data-delta":"7"},"fields":{}}]]

4. Durham Innovation District (“Durham.ID”)

Durham Innovation District is a master planned research hub for downtown Durham led by Longfellow Real Estate Partners, Hank Scherich (CEO of Measurement Inc.) and Duke University. Durham.ID covers 15 acres and eventually will include over 1.48 million SF of both new and existing office and lab space as well as 50,000 SF of retail, 300 new residential units and three parking decks. Duke University is already located in the Carmichael Building and is expected to lease additional space within Durham.ID. The development plans to function as a research hub with emphasis on life science companies and researchers looking to collaborate with each other and Duke University. The project is estimated to cost $400-$500 million.

Source: Cushman & Wakefield

| Property | Sale Date | Size (Square Feet) | Price | $/Square Foot | Cap Rate | |

|---|---|---|---|---|---|---|

| Rogers Alley | Dec-14 | 30,000 | $6,100,000 | $203 | 6.30% | |

| American Tobacco Hall | Dec-14 | 71,600 | $14,400,000 | $201 | 7.25% | |

| Venable Center | Jan-16 | 85,886 | $18,000,000 | $210 | N/A | |

| 211 Rigsbee Avenue | Oct-15 | 7,920 | $1,435,000 | $181 | 6.50% | |

| Average | 48,852 | $14,182,539 | $204 | 6.68% | ||

| Subject | 27,691 | $6,100,000 | $220 | 8.29% | ||

| Property | Size (Square Feet) | Rental Rate | Year Built | Lease Type |

|---|---|---|---|---|

| 405 E. Chapel Hill Street | 1,395 | $24.00 | 1920 | NNN |

| 206-208 Rigsbee Avenue | 3,882 | $26.00 | 1912 | NNN |

| 401 E. Chapel Hill Street | 3,000 | $24.50 | 1922 | NNN |

| 125 E. Parish Street | 1,636 | $23.47 | 1910 | NNN |

| 353 W. Main Street | 577 | $22.88 | 1920 | NNN |

| Average | 2,098 | $24.17 | 1917 | NNN |

| Subject - Pro Forma Rents | N/A | $21.00 | 1930 & 1932 | NNN |

The comparables included in the above tables were either sourced from CoStar, Real Capital Analytics or they were provided by the Sponsor

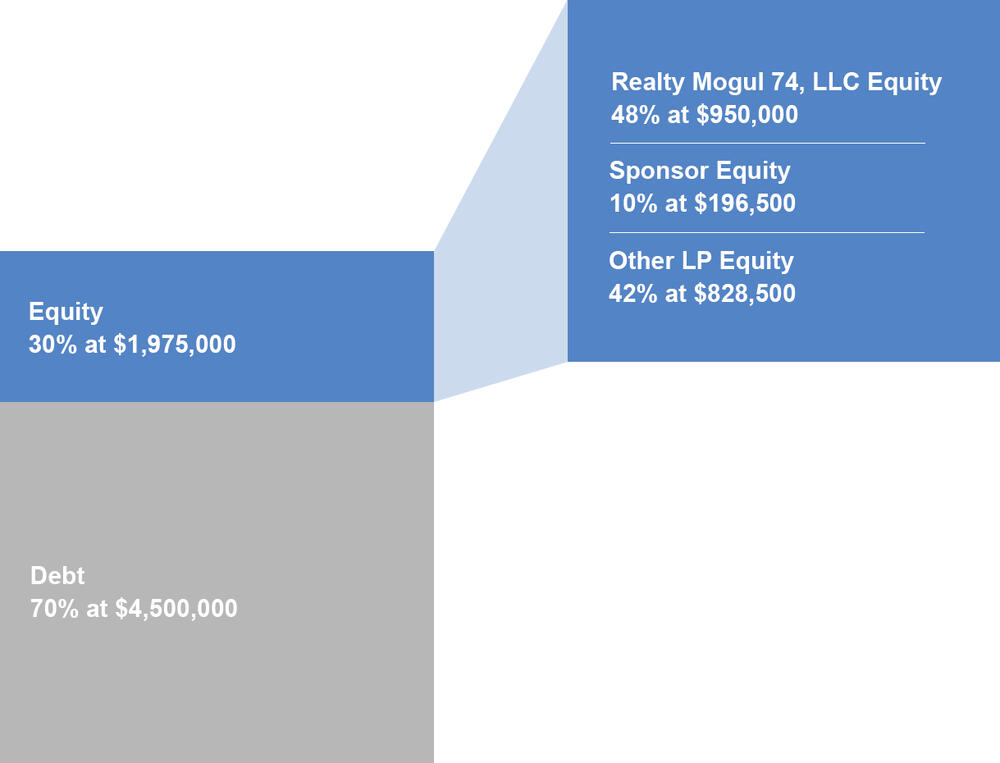

| Sources of Funds | ||

| Debt | $4,500,000 | |

| Equity | $1,975,000 | |

| Total Sources of Funds | $6,475,000 | |

| Uses of Funds | ||

| Purchase Price | $6,100,000 | |

| Acquisition Fee | $61,000 | |

| Broker-Dealer Fee | $40,000 | |

| Closing Costs and Fees | $122,250 | |

| Hard Costs | $30,750 | |

| Tenant Improvement/Leasing Commission Reserve | $121,000 | |

| Total Uses of Funds | $6,475,000 | |

The projected terms of the debt financing are as follows:

- Lender: AloStar Bank of Commerce

- Proceeds: $4,500,000

- Interest Rate: One-Month Libor + 325 bps Floating

- Amortization: 25 years, with three (3) years of interest only

- Term: Five (5) years

- Extension Option: None

- Recourse: 7% of the loan amount ($315,000) to the Sponsors

- Exit Fee: $15,000

There can be no assurance that a lender will provide debt on the rates and terms noted above, or at all. All rates and terms of the debt financing are subject to lender approval, including but not limited to possible increases in capital reserve requirements for funds to be held in a lender controlled capital reserve account.

Foster Retail, LLC intends to make distributions to Investors (Realty Mogul 74, LLC, other LP investors, and Sponsor, collectively, the "Members" or "Member") per the priority order below.

- First, 100% of all distributable cash flow to Members pari passu until return of capital contributions;

- Second, 100% pari passu to Members until each Member receives cash in the aggregate to constitute an 8% internal rate of return (“IRR”);

- Third, 30% to Members and 70% to the Sponsor until the Sponsor has received cash in the aggregate equal to 30% of the amount by which all distributable cash exceeds all capital contributions (the “Catch Up”);

- Thereafter, 70% to the Members pro rata and 30% to the Sponsor.

Distributions are expected to start in August 2017 and are anticipated to continue on a quarterly basis thereafter. Note that the return of initial capital occurs only upon a capital event (sale or refinance). These distributions are at the discretion of the Sponsor, who may decide to delay distributions for any reason, including maintenance or capital reserves. Realty Mogul 74, LLC is to distribute 100% of its share of excess cash flow (after expenses and fees) to the Members of Realty Mogul 74, LLC (the RealtyMogul.com investors).

| Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | |

|---|---|---|---|---|---|

| Effective Gross Revenue | $779,639 | $879,026 | $910,118 | $936,434 | $963,006 |

| Total Operating Expenses | $312,880 | $349,092 | $357,771 | $375,956 | $385,827 |

| Net Operating Income | $466,759 | $529,934 | $552,347 | $560,478 | $577,179 |

| Distributions to Realty Mogul 74, LLC Investors | $71,843 | $75,819 | $76,375 | $37,665 | $1,512,844 |

Certain fees and compensation will be paid over the life of the transaction. The following fees and compensation will be paid:

| Type of Fee | Amount of Fee | Received By | Paid From | Notes |

|---|---|---|---|---|

| One-Time Fees | ||||

| Acquisition Fee | $61,000 | Sponsor | Capitalized Equity Contribution | 1.0% of the Property purchase price |

| Broker-Dealer Fee | $40,000 | North Capital (1) | Capitalized Equity Contribution | 4.0% based on the amount of equity invested by Realty Mogul 74, LLC with a minimum of $40,000 |

| Leasing Commissions | 3% New / 2% Renewal | Sponsor | Operating Cash Flow | |

| Recurring Fees | ||||

| Property Management Fee | 3.0% of effective gross income | Sponsor | Operating Cash Flow | 3.0% of effective gross income |

| Asset Management Fee | $19,750 per year | Sponsor | Operating Cash Flow | 1.0% of invested equity |

| Management and Administrative Fee | 1.0% of investment assets in Realty Mogul 74, LLC | RM Manager, LLC | Distributable Cash | RM Manager, LLC is the Manager of Realty Mogul 74, LLC and a wholly-owned subsidiary of Realty Mogul, Co. (2) |

Notes:

(1) Certain employees of Realty Mogul, Co. are also registered representatives of, and are paid commissions by, North Capital Private Securities Corporation, a Delaware Corporation ("North Capital"). In addition, North Capital pays a technology provider services fee to Realty Mogul Co. for licensing and access to certain technology, reporting, communications, branding, entity formation and administrative services performed from time to time by Realty Mogul, Co., and North Capital, Co. are parties to a profit sharing arrangement.

(2) Fees may be deferred to reduce impact to investor distributions.

The above presentation is based upon information supplied by the Sponsors. Realty Mogul, Co., RM Manager, LLC, and Realty Mogul 74, LLC, along with their respective affiliates, officers, directors or representatives (the "RM Parties") hereby advise you that none of them has independently confirmed or verified any of the information contained herein. The RM Parties further make no representations as to the accuracy or completeness of any such information and undertake no obligation now or in the future to update or correct this presentation or any information contained herein.

The information on this Page is qualified in its entirety by reference to the more complete information about the offering contained in the Sponsor’s Investment Documents. The information on this Page is not complete and subject to change at the Sponsor’s discretion at any time up to the closing date. The Sponsor’s Investment Documents and supplements thereto contain important information about the Sponsor’s offering including relevant investment objectives, the business plan, risks, charges, expenses, and other information, which you should consider carefully before investing. The information on this Page should not be used as a basis for an investor’s decision to invest.

Risk of InvestmentThis investment is speculative, highly illiquid, and involves substantial risk. There can be no assurances that all or any of Sponsor’s assumptions, expectations, estimates, goals, hypothetical illustrations, or other aspects of Sponsor’s business plans (“Assumptions”) will be true or that actual performance will bear any relation to Sponsor’s Assumptions, and no guarantee or representation is made that Sponsor’s Assumptions will be achieved. If Sponsor does not achieve its Assumptions, your investment could be materially and adversely affected. A loss of part or all of the principal value of your investment may occur. You should not invest unless you can readily bear the consequences of such loss. Sponsor’s Assumptions should not be relied upon as the primary basis for your decision to invest.

No Reliance on Forward-Looking Statements; Sponsor AssumptionsSponsor is solely responsible for statements made concerning forward-looking statements and Assumptions, which apply only as of the date made, are preliminary and subject to change, and are expressly qualified in their entirety by the disclosures and cautionary statements included in Sponsor’s Investment Documents, which you should carefully review. Sponsor is obligated to update or revise such forward-looking statements or Assumptions to reflect events or circumstances that arise after the date made or to reflect the occurrence of unanticipated events. Sponsor’s forward-looking statements and Assumptions are hypothetical, not based on actual investment achievements or events, and are presented solely for purposes of providing insight into the Sponsor’s investment objectives, detailing Sponsor’s anticipated risk and reward characteristics, and establishing a benchmark for future evaluation of actual results; therefore, they are not a predictor, projection, or guarantee of future results. You should not rely on Sponsor’s forward-looking statements as a basis to invest.

Importantly, we do not adopt, endorse, or provide any assurance of returns or as to the accuracy or reasonableness of Sponsor’s Assumptions or forward-looking statements.

No Reliance on Past PerformanceAny description of past performance is not a reliable indicator of future performance and should not be relied upon as the primary basis to invest.

Sponsor’s Use of DebtA substantial portion of the total cost of the real estate asset acquired by the Sponsor with investor funds (“Property”) will be paid with borrowed funds, i.e., debt. Sponsor’s estimated rates and terms of the debt financing are subject to lender approval, and there is no assurance that the Sponsor will secure debt at the rates and terms presented on this Page or in the Sponsor’s Investment Documents, or at all. The use of borrowed money to acquire real estate is referred to as leveraging, which can amplify losses and could result in lender foreclosure. In addition, if the debt includes a variable (or “floating”) interest rate, the total amount of interest paid over the term of the debt will fluctuate and can increase. As a result, Sponsor’s use of debt can result in a loss of some or all of your investment.

Sponsor’s Offering is Not RegisteredSponsor’s securities offering will not be registered under the Securities Act of 1933, as amended (the “Securities Act”), in reliance upon the exemptions from registration pursuant to Rule 506(c) of Regulation D as promulgated under the Securities Act (“Private Placement”). In addition, the offering will not be registered under any state securities laws in reliance on exemptions from state registration. Such securities (your ownership interests) are subject to restrictions on transferability and resale and may not be transferred or resold except as permitted under applicable state and federal securities laws pursuant to registration or an available exemption. All Private Placements on the Platform are intended solely for “Accredited Investors,” as that term is defined in Rule 501(a) under the Securities Act.

No Investment AdviceNothing on this Page should be regarded as investment advice (either with respect to a particular security or regarding an overall investment strategy), a recommendation, an offer to sell, or a solicitation of or an offer to buy any security. Advice from a securities professional is strongly advised to understand and assess the risks associated with real estate or private placement investments.

1031 Exchange RiskInternal Revenue Code Section 1031 (“Section 1031”) contains complex tax concepts and certain tax consequences may vary depending on the individual circumstances of each investor. You should consult with and rely on your own tax advisor about the tax aspects with respect to your particular circumstances.