DSW Commercial

DSW was established in Tucson, Arizona by Michael Sarabia (DSW Commercial Principal) and Mark Schnuck (DESCO Group Principal) in 2001 as a full service commercial real estate firm in partnership with The DESCO Group, a leading development, property management and investment company based in St. Louis, Missouri. DSW Commercial Real Estate (formerly DESCO Southwest) began to build alliances with Arizona brokers and identified investment and development opportunities in the Tucson and Phoenix markets.

DSW Commercial Real Estate has developed several successful projects in the Arizona Market with projects such as the Skyline Esplanade office complex in Tucson, the unique redevelopment of the Phoenix Union High School in downtown Phoenix as a facility to accommodate the University of Arizona College of Medicine, and the construction of the Stapley Corporate Center in Mesa, Arizona. DSW Commercial Real Estate has developed approximately 1,000,000 square feet of office, medical and retail space.

In 2016, Michael Sarabia and James Hardman negotiated the purchase of the operating platform for DSW Commercial Real Estate from the DESCO Group to continue to develop and invest in commercial real estate and operate the property management and brokerage business independent from the DESCO Group. Since that time, DSW Commercial Real Estate has invested in nearly $125 million dollars of commercial real estate. Currently, DSW Commercial Real Estate manages over one million square feet of office, medical and retail real estate and is currently developing a number of office, medical and retail centers.

Deloache Capital

Deloache Capital (“Deloache”) is a commercial real estate (“CRE”) finance company that is currently deploying capital for Deloache Capital Fund I (the “Fund”). The Fund is making investments in and providing liquidity for, commercial real estate assets. Their investment philosophy is simple: find great people, provide capital into the right structure and find strong potential in the real estate. Deloache was founded as a collaboration between highly successful institutions: Thomas Title & Escrow (“Thomas Title”) and Presidium Group (“Presidium”). Thomas Title is a leading commercial real estate title insurance agency. Established in 2006, Thomas Title has closed over $30 billion in CRE transaction volume. Frank Busch is the Founder of Thomas Title and serves as the Managing Principal of Deloache. On June 1, 2021, Thomas Title was sold to Stewart Title (NYSE:STC), and Frank Busch remains the CEO of Thomas Title. Presidium is a large CRE development company that has deployed over $4 billion in such transactions generating a 2.9x cash-on-cash return for a 40% Gross IRR on over $1 billion of realized investments. Presidium’s Co-CEOs John Griggs and Cross Moceri are Principals of Deloache. The Fund’s General Partner (“GP”) has committed to investing $3 million of the Fund’s capital commitments. Deloache has deep expertise in the rental housing sector.

https://www.deloachecapital.com/

G.S. Jaggi

One of DSW's top investor partners, G.S. Jaggi, is involved in these projects. Jaggi is considered one of the early pioneers of build-for-rent housing. G.S. Jaggi has 20 years of entrepreneurial experience and founded Iridius Capital in 2011 to bring Avilla Homes communities to market. Under Mr. Jaggi’s leadership, Iridius’ portfolio has grown to include multifamily, office, retail, and hotel properties. Mr. Jaggi has overseen the acquisition and/or development of over one billion dollars in real estate assets. Prior to founding Iridius Capital, Mr. Jaggi was the founder and CEO of one of the largest privately-held mortgage banks in the United States.

DSW's three La Vida projects are build-for-rent communities ranging from 29 doors to 46 doors. Located in prime locations in Tucson, these projects are completely surrounded by quality residential housing with very low vacancy (4-5% approximately). All projects are completely entitled and are shovel-ready. The build-for-rent housing sector is considered to be one of the hottest investments in real estate today. One of DSW's top investor partners, G.S. Jaggi, is involved in these projects. Jaggi is considered one of the early pioneers of build-for-rent housing.

River 1

| Floor Plan | # of Units | Avg SF/Unit | $ / Unit | $ / SF | % of Total |

| River 1 2x2 | 12 | 1,026 | $1,621 | $1.58 | 41% |

| River 1 3x2 | 17 | 1,187 | $1,911 | $1.61 | 59% |

| Total/Averages | 29 | 1,120 | $1,791 | $1.60 | 100% |

River 2

| Floor Plan | # of Units | Avg SF/Unit | $ / Unit | $ / SF | % of Total |

| River 2 2x2 | 15 | 1,026 | $1,652 | $1.61 | 33% |

| River 2 3x2 | 31 | 1,187 | $1,935 | $1.63 | 67% |

| Total/Averages | 46 | 1,135 | $1,843 | $1.62 | 100% |

River 3

| Floor Plan | # of Units | Avg SF/Unit | $ / Unit | $ / SF | % of Total |

| Civano 2x2 | 9 | 1,026 | $1,611 | $1.57 | 33% |

| Civano 3x2 | 18 | 1,187 | $1,899 | $1.60 | 67% |

| Total/Averages | 27 | 1,133 | $1,803 | $1.59 | 100% |

Combined

| # of Units | Avg SF/Unit | $ / Unit | $ / SF | |

| Total/Averages | 102 | 1,130 | $1,817 | $1.61 |

Lease Comparables

| Avilla River | The Hedrick on Mountain | McCormick Urban Living | Avila Tanque Verde | Sabino Vista | Averages | Subject | |

| Year Built | 2013 | 2020 | 2017 | 2011 | 2014 | 2015 | 2022 |

| # of Units | 76 | 60 | 25 | 85 | 53 | 60 | 102 |

| Average Rental Rate | $1,764 | $1,743 | $2,035 | $1,794 | $2,129 | $1,893 | $1,817 |

| Average Unit Size | 984 SF | 1,000 SF | 1,289 SF | 971 SF | 1,102 SF | 1,069 SF | 1,130 SF |

| Average $/SF | $1.79/SF | $1.74/SF | $1.58/SF | $1.85/SF | $1.93/SF | $1.78/SF | $1.61/SF |

| Distance from subject | 0.1 mi | 3.5 mi | 5.4 mi | 7.9 mi | 9.6 mi | ||

| $/Unit (2x2) | $1,751 | $1,660 | $1,815 | $1,775 | $1,949 | $1,790 | $1,631 |

| SF (2x2) | 965 SF | 900 SF | 1,142 SF | 922 SF | 965 SF | 979 SF | 1,026 SF |

| $/SF (2x2) | $1.81/SF | $1.84/SF | $1.59/SF | $1.93/SF | $2.02/SF | $1.84/SF | $1.59/SF |

| $/Unit (3x2) | $1,991 | $1,868 | $2,139 | $2,049 | $2,315 | $2,072 | $1,919 |

| SF (3x2) | 1,244 SF | 1,150 SF | 1,358 SF | 1,244 SF | 1,244 SF | 1,248 SF | 1,187 SF |

| $/SF (3x2) | $1.60/SF | $1.62/SF | $1.58/SF | $1.65/SF | $1.86/SF | $1.66/SF | $1.62/SF |

Sales Comparables

| McCormick Urban Living | Galeria del Rio | Averages | Subject | |

| Date Sold | 7/1/2021 | 2/1/2020 | July 2023 | |

| Year Built | 2014 | 2017 | 2016 | 2022 |

| # of Units | 101 | 25 | 63 | 102 |

| Average Unit Size | 1,573 SF | 1,289 SF | 1,431 SF | 1,130 SF |

| Sale Price | $32,025,000 | $8,150,000 | $20,087,500 | $34,783,036 |

| $/Unit | $317,079 | $326,000 | $321,540 | $341,010 |

| $/SF | $202/SF | $253/SF | $227/SF | $302/SF |

| Building Size | 158,870 SF | 32,222 SF | 95,546 SF | 115,278 SF |

| Distance from subject | 0.9 mi | 5.4 mi | 3.2 mi |

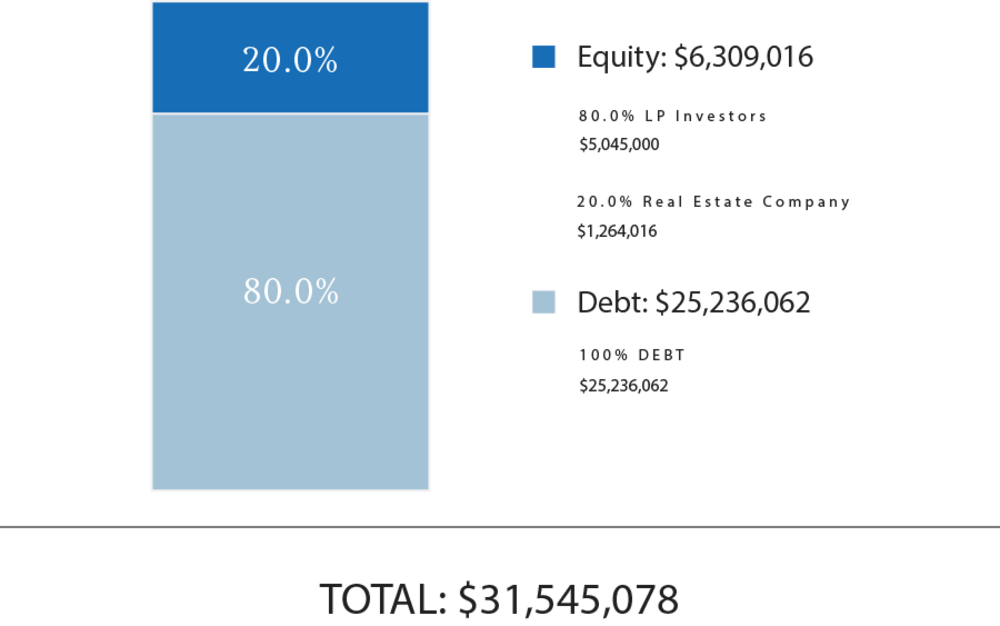

Total Capitalization

| Sources of Funds | $ Amount | $/Unit |

| Debt | $25,236,062 | $247,412 |

| GP Investor Equity | $1,264,016 | $12,392 |

| LP Investor Equity | $5,045,000 | $49,461 |

| Total Sources of Funds | $31,545,078 | $309,265 |

| Uses of Funds | $ Amount | $/Unit |

| Land Acquisition Cost | $2,322,449 | $22,769 |

| Closing Costs* | $2,290,582 | $22,457 |

| Hard Costs | $22,751,262 | $223,052 |

| Soft Costs | $3,190,034 | $31,275 |

| Reserve | $990,751 | $9,713 |

| Total Uses of Funds | $31,545,078 | $309,265 |

The Sponsor’s equity contribution may consist of friends and family equity and equity from funds controlled by the Sponsor.

(1) RM Technologies, LLC, an affiliate of RealtyMogul, operates the RealtyMogul Platform. RM Technologies, LLC charges a fixed, non-percentage-based fee for real estate companies and their sponsors to use the Platform and for Platform-related services. Please see the Fees and Disclaimers sections below for additional information concerning fees paid to RM Technologies, LLC.

The expected terms of the debt financing are as follows:

- Lender: Trez Capital

- Term: 16 months commencing from the Interest Adjustment Date

- Loan to Cost: 80.0%

- Estimated Proceeds: $25,236,062

- Interest Type: Floating

- Spread Above One-Month LIBOR: 4.25% over the Wall Street Journal Prime Rate (WSJ) per annum, payable monthly and calculated on a 365 day basis with a floor rate of 7.5%

- Interest-Only Period: Full-term

- Amortization: N/A

- Prepayment Terms: N/A

- Extension Requirements: Borrower may request, within sixty (60) days notice of expiration of the Term, two (2) six (6) months extension options, subject to the satisfaction of customary extension conditions, including, without limitation to:

a. Payment of 0.5% of the outstanding balance for the first Extension Option and 0.5% of the outstanding balance for the second Extension Option;

b. LTV at completion to be no more than 76% of the stabilized value as determined by the Lender;

c. No Event of Default shall exist, and no event shall have occurred and no condition shall exist which, after notice or lapse of time, or both, would constitute an Event of Default.

There can be no assurance that the Sponsor will secure debt on the rates and terms noted above, or at all. All of the Sponsor’s estimated rates and terms of the debt financing are subject to lender approval, including but not limited to possible increases in capital reserve requirements for funds to be held in a lender-controlled capital reserve account.

A substantial portion of the total acquisition for the Property will be paid with borrowed funds. The use of borrowed money to acquire real estate is referred to as leveraging. Leveraging increases the risk of loss. If the Sponsor were unable to pay the payments on the borrowed funds (called a "default"), the lender might foreclose, and the Sponsor could lose its investment in its property.

DSW intends to make distributions as follows:

- To the Investors, pari passu, all operating cash flows to a 10.0% IRR;

- 65% / 35% (65% to Investors / 35% to Promote/Carried Interest) of excess cash flow to a 20.0% IRR;

- 50% / 50% (50% to Investors / 50% to Promote/Carried Interest) of excess cash flow thereafter.

DSW intends to make distributions to investors after the payment of the company's liabilities (loan payments, operating expenses, and other fees as more specifically set forth in the LLC agreements, in addition to any member loans or returns due on member loan).

Distributions are expected to start in February 2024 and are projected to continue on a quarterly basis thereafter. Distributions are at the discretion of DSW, who may decide to delay distributions for any reason, including maintenance or capital reserves.

DSW will receive a promoted/carried interest as indicated above, and a portion of this promoted/carried interest may be received by RM Admin, LLC.

| Cash Flow Summary | |||||

| Year 1 | Year 2 | ||||

| Effective Gross Revenue | $39,988 | $2,033,941 | |||

| Total Operating Expenses | $70,448 | $374,618 | |||

| Net Operating Income | ($30,460) | $1,659,323 | |||

| Project-Level Cash Flows | |||||

| Year 0 | Year 1 | Year 2 | |||

| Net Cash Flow | ($6,309,016) | $0 | $9,597,349 | ||

| Investor-Level Cash Flows(1) | |||||

| Year 0 | Year 1 | Year 2 | |||

| Net Cash Flow | ($5,045,000) | $0 | $7,122,147 | ||

| Investor-Level Cash Flows - Hypothetical $50,000 Investment(1) | |||||

| Year 0 | Year 1 | Year 2 | |||

| Net Cash Flow | ($50,000) | $0 | $70,586 | ||

(1) Returns are net of all fees. Such Fees include fees paid to RM Admin, an affiliate of RealtyMogul, who charges an annual fixed administrative fee for providing certain ongoing administrative services to the Sponsor. Please see the Fees and Disclaimers sections and Disclaimers sections below for additional information concerning fees paid to RM Admin.

RM Technologies, LLC and its affiliates does not provide any assurance of returns. The content on this Page, including Sponsor’s pro forma projections, was provided by the Sponsor or an affiliate thereof. Although RM Technologies, LLC believes the Sponsor reliably produced this content, RM Technologies, LLC makes no representations or warranties as to the accuracy of such information and accepts no liability therefor. The assumptions and projections included in the content on this Page, including the Sponsor’s pro forma projections, are not reflective of the position of RM Technologies, LLC or any other person or entity other than the Sponsor or its affiliates. There can be no assurances that all or any of the Sponsor’s assumptions will be true, that actual performance will bear any relation to these hypothetical illustrations, or that the Sponsor’s investment objectives will be achieved. For additional information concerning the Sponsor’s assumptions and projections, and the significant risks involved in investing in real estate, please see the Disclaimers section below.

Certain fees and compensation will be paid over the life of the transaction; please refer to DSW's materials for details. The following fees and compensation will be paid(1)(2)(3)(4):

| One-Time Fees: | |||

| Type of Fee | Amount of Fee | Received By | Paid From |

| Developer Fee | 1.5% of the hard cost for River 1 and River 2, 3.0% of the hard cost for Civano | DSW | Capitalization |

| Acquisition Fee | 2.0% of the Land Purchase Price | DSW | Capitalization |

| Loan Guarantee Fee | 2.0% of Loan Proceeds | G.S. Jaggi | Capitalization |

| Recurring Fees: | |||

| Type of Fee | Amount of Fee | Received By | Paid From |

| Administrative Services Fee | 1.0% of Equity Invested(1) | RM Admin(3) | Cash Flow |

| Asset Management Fee | 1.0% of Invested Capital | DSW | Cash Flow |

(1) Only applies to equity raised through the RealtyMogul Platform

(2) Fees may be deferred to reduce impact to investor distributions.

(3) RM Technologies, LLC, an affiliate of RealtyMogul, operates the RealtyMogul Platform. RM Technologies, LLC charges a fixed, non-percentage-based fee for real estate companies and their sponsors to use the RM Technologies, LLC’s proprietary Platform and receive Platform-related services. An estimate of this fee is included in the Closing Costs above and is intended to be capitalized into the transaction at the discretion of the Sponsor. The Platform fees received by RM Technologies, LLC are disclosed in the relevant operating agreement(s). RM Technologies LLC’s receipt of Platform fees creates a conflict of interest between RealtyMogul and its affiliates, and investors or prospective investors.

(4) RM Admin, an affiliate of RealtyMogul, charges an annual fixed administrative fee for providing certain ongoing administrative services to the Sponsor. RM Admin’s administrative services and fees are disclosed in the relevant operating agreement(s). RM Admin’s receipt of administrative fees creates a conflict of interest between RealtyMogul and its affiliates, and investors or prospective investors.

The information on this Page is qualified in its entirety by reference to the more complete information about the offering contained in the Sponsor’s Investment Documents. The information on this Page is not complete and subject to change at the Sponsor’s discretion at any time up to the closing date. The Sponsor’s Investment Documents and supplements thereto contain important information about the Sponsor’s offering including relevant investment objectives, the business plan, risks, charges, expenses, and other information, which you should consider carefully before investing. The information on this Page should not be used as a basis for an investor’s decision to invest.

Risk of InvestmentThis investment is speculative, highly illiquid, and involves substantial risk. There can be no assurances that all or any of Sponsor’s assumptions, expectations, estimates, goals, hypothetical illustrations, or other aspects of Sponsor’s business plans (“Assumptions”) will be true or that actual performance will bear any relation to Sponsor’s Assumptions, and no guarantee or representation is made that Sponsor’s Assumptions will be achieved. If Sponsor does not achieve its Assumptions, your investment could be materially and adversely affected. A loss of part or all of the principal value of your investment may occur. You should not invest unless you can readily bear the consequences of such loss. Sponsor’s Assumptions should not be relied upon as the primary basis for your decision to invest.

No Reliance on Forward-Looking Statements; Sponsor AssumptionsSponsor is solely responsible for statements made concerning forward-looking statements and Assumptions, which apply only as of the date made, are preliminary and subject to change, and are expressly qualified in their entirety by the disclosures and cautionary statements included in Sponsor’s Investment Documents, which you should carefully review. Sponsor is obligated to update or revise such forward-looking statements or Assumptions to reflect events or circumstances that arise after the date made or to reflect the occurrence of unanticipated events. Sponsor’s forward-looking statements and Assumptions are hypothetical, not based on actual investment achievements or events, and are presented solely for purposes of providing insight into the Sponsor’s investment objectives, detailing Sponsor’s anticipated risk and reward characteristics, and establishing a benchmark for future evaluation of actual results; therefore, they are not a predictor, projection, or guarantee of future results. You should not rely on Sponsor’s forward-looking statements as a basis to invest.

Importantly, we do not adopt, endorse, or provide any assurance of returns or as to the accuracy or reasonableness of Sponsor’s Assumptions or forward-looking statements.

No Reliance on Past PerformanceAny description of past performance is not a reliable indicator of future performance and should not be relied upon as the primary basis to invest.

Sponsor’s Use of DebtA substantial portion of the total cost of the real estate asset acquired by the Sponsor with investor funds (“Property”) will be paid with borrowed funds, i.e., debt. Sponsor’s estimated rates and terms of the debt financing are subject to lender approval, and there is no assurance that the Sponsor will secure debt at the rates and terms presented on this Page or in the Sponsor’s Investment Documents, or at all. The use of borrowed money to acquire real estate is referred to as leveraging, which can amplify losses and could result in lender foreclosure. In addition, if the debt includes a variable (or “floating”) interest rate, the total amount of interest paid over the term of the debt will fluctuate and can increase. As a result, Sponsor’s use of debt can result in a loss of some or all of your investment.

Sponsor’s Offering is Not RegisteredSponsor’s securities offering will not be registered under the Securities Act of 1933, as amended (the “Securities Act”), in reliance upon the exemptions from registration pursuant to Rule 506(c) of Regulation D as promulgated under the Securities Act (“Private Placement”). In addition, the offering will not be registered under any state securities laws in reliance on exemptions from state registration. Such securities (your ownership interests) are subject to restrictions on transferability and resale and may not be transferred or resold except as permitted under applicable state and federal securities laws pursuant to registration or an available exemption. All Private Placements on the Platform are intended solely for “Accredited Investors,” as that term is defined in Rule 501(a) under the Securities Act.

No Investment AdviceNothing on this Page should be regarded as investment advice (either with respect to a particular security or regarding an overall investment strategy), a recommendation, an offer to sell, or a solicitation of or an offer to buy any security. Advice from a securities professional is strongly advised to understand and assess the risks associated with real estate or private placement investments.

1031 Exchange RiskInternal Revenue Code Section 1031 (“Section 1031”) contains complex tax concepts and certain tax consequences may vary depending on the individual circumstances of each investor. You should consult with and rely on your own tax advisor about the tax aspects with respect to your particular circumstances.